CKBlog: The Market

Monday, July 31, 2017

2017 Semi-Annual Review

by Charlie Haberstroh, CEO & CIO

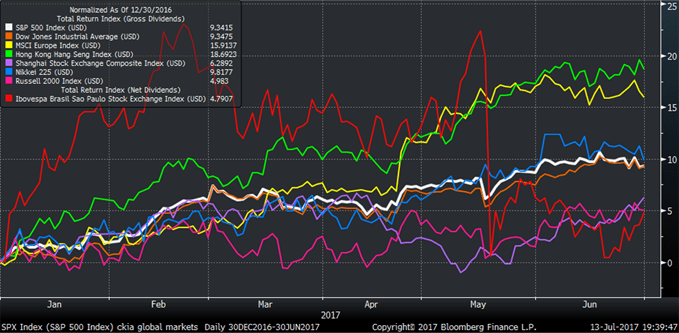

Equity Markets’ Total Returns Year-to-Date through June 30, 2017 in US Dollar terms:

- S&P 500: +9.34%

- Dow Jones: +9.35%

- MSCI Europe Index: +15.91%

- Hang Seng Index: +18.69%

- Shanghai Composite: +6.29%

- Nikkei 225: +9.82%

- Russell 2000: +4.98%

- IBOVESPA: +4.79%

*Total Return (includes dividends); the IBOVESPA does not include dividends.

Commentary from our CIO

It is impossible to avoid discussions about the Trump Administration in everyday life. So why should our semi-annual review be any different? I promise any political discussion will be in the context of market dynamics. It will be brief.

If someone stood before you on December 31, 2016 and told you that by June 30th, 2017 the S&P 500 Index would be up +9.34% including dividends, you’d likely have assumed that the Trump administration accomplished several key aspects of their “Pro Business” agenda. You might have expected that major tax reforms were passed, regulations were slashed, an infrastructure bill was moving through Congress and a reasonable solution to the Affordable Health Care Act was achieved. You’d be wrong.

In fact, despite the stalemate and dysfunction in Washington, D.C., the S&P 500 Index is up +14.74% since Trump was elected through June 30th 2017. So if the US stock market performance cannot be attributed pro-business legislation, what can we point to?

- Corporate Profits Remain Strong: FactSet estimates that Q2 year over year S&P 500 earnings will increase by more than 6%.

- Petroleum Prices Remain Low: While a drop in oil and gas prices will hurt oil company profits (in the short run), lower oil and gas prices have a stimulative effect on the largest part of the US economy; the consumer.

- A Weakening US Dollar: Many patriots argue a strong dollar is good for the US. But the same cannot be said for most of the constituents in the S&P 500 Index. Many companies headquartered in the US generate a majority of their revenue from outside of the US. Even NETFLIX recently reported that non-US folks now make up more than half of their subscribers. For these types of companies, a lower USD can have a positive effect on earnings.

- GDP Growth: The US economy continues to expand (albeit at a snail’s pace) with no clear signs of recessionary indicators.

But it’s not all rosy.

- Geopolitical Tensions: Developments in North Korea, Russia, the Middle East (ISIS) and even China give investors pause. Geopolitical risks will never go away. Prudent stewards of capital will always keep a watchful eye.

- Washington D.C.: Tensions are hot. Nothing is getting done. But things can always get worse. The debate over Obamacare is fierce. The chatter about the impending Debt Limit is increasing and the word “impeachment” is back in the headlines.

- Fed Rate Increases: Most analysts believe the Fed will increase rates twice more this year. Rate increases historically have been headwinds for the stock market.

- Equity Valuations seem Fully Valued: By most ratios and historical analysis, the US Stock market valuation is currently above average and we have not experienced more than a handful of sell-offs over the last eight years. As this positive trend continues, the probability of a sell-off increases.

So what are stock investors to do?

Just because the overall stock market may be sitting at lofty valuations, it does not mean pockets of value cannot be found. Speaking of value, the S&P 500 Value Index is only up +3.89% including dividends for the first half of 2017. This compares to +12.44% for its growth counterpart. Many of our value managers tell us their portfolio companies are cheap and have room to run.

Smaller company stocks have not kept pace with larger company stocks. The Russell 2000 Index is only up +4.98% including dividends through June 30th. If Trump is successful in slashing regulations and lowering taxes, smaller US companies should benefit.

If you are concerned about the political climate and equity valuations in the U.S., look elsewhere. We’ve been allocating to European equities for several years and it has paid off so far this year. The MSCI European Index is up +15.91% in USD terms YTD through June 30th, and its estimated P/E Ratio is more than 15% cheaper than the estimated P/E Ratio of the S&P 500 Index. Several of our active managers operating in this space continue to outperform their benchmarks in Europe. Sure, European equities have been “hotter” than US equities this year, but they remain cheaper too.

Europe isn’t the only region outperforming the US equity markets. Despite all of the challenges facing emerging market countries, their collective stock markets have also been strong this year. The iShares MSCI Emerging Markets ETF (ticker EEM) was up +18.78% including dividends through June 3Oth. If you’d like to have exposure to emerging markets but you cannot stomach the volatility of countries such as Brazil, Argentina, Russia, India, and China, be comforted that many US multinational companies sell products and services into these countries. So if you own companies in the S&P 500 Index, chances are you have underlying exposure to the emerging markets.

What About Bonds?

For several years now, we’ve been concerned about the risk versus potential reward for fixed income in general. And for several years now, fixed income returns continued to chug along, far outpacing the paltry returns of cash and cash equivalents. The Barclays US Aggregate Total Return Index (a common benchmark for bonds) is up +4.32% through June 30th and has averaged up +4.02% per year over the last five years.

While we may not be particularly sanguine about bonds in general today, prudent asset allocation does in fact call for allocations to bonds. In general, when allocating to bonds, we prefer short duration securities or bonds whose coupons are indexed to prevailing interest rates. Both should offer protection should interest rates continue to increase (and therefore push bond prices lower).

A Quick Note on Cash

With the recent Fed Rate increases, our performance reports are starting to show that cash positions have been positive contributors to portfolio performance. In past years, allocations to cash returned virtually zero. But as rates continue to rise (if they do), not only will this benefit individual investors who hold cash in their portfolio, but banks, custodians, brokers and mutual fund companies should also see cash finally add to their bottom line.

Speaking of the Bottom Line ...

While the S&P 500 Index and the Dow Jones Industrial Index are at or near all-time highs, certain segments and regions of global stock markets remain undervalued and attractive. Despite our lack of excitement regarding the prospects of fixed income in general, bonds will continue to play a role in portfolio construction. Investors should revisit how they are allocating to both stocks and bonds.

A Very Important Note about CastleKeep

As of July 1, 2017, I am pleased to announce that two of my sons, Chuck and Steve, are now partners of CastleKeep. This process started back in the early days when both worked as summer interns and was recently solidified as we developed a succession plan to guide CastleKeep into the next 50 years. I am a very proud father, boss, and now co-owner.